A couple of weeks ago Barcelona and Real Madrid produced an enthralling 2-2 draw in El Clásico with two goals apiece from their superstars Lionel Messi and Cristiano Ronaldo. It seemed appropriate that the latest match in a series of titanic struggles finished level, as there has been little to separate the two Spanish giants recently.

Their dominance in La Liga has become unquestioned, as they have shared the last eight league titles between them, Barcelona winning five times, while Madrid have been victorious on three occasions, including last season. In Europe, Barcelona have led the way, winning the Champions League twice in the last four years. Although Madrid have not been quite so prominent recently, they have reached the semi-finals of the last two tournaments, and they have won the trophy more than any other club (nine times).

"Xavi - little triggers"

Despite an uncharacteristically nervous start to the season by these two powerhouses, few would bet against La Liga once again turning into a two-horse race. Indeed, when questioned about Malaga’s potential, their exciting young star Isco’s downbeat response spoke for many, “Atlético Madrid and ourselves have begun well, but there are two teams superior to the rest and there are no others that can fight them for the title.”

They also appear to be doing fantastically well off the pitch, both reporting revenues of around half a billion Euros for the 2011/12 season. More importantly, both clubs registered hefty profits: Barcelona’s €49 million was their all-time record, while Madrid’s €32 million was also a notable achievement. Equally significantly, they have also been reducing their sizeable debts to a more manageable level.

In fact, Madrid claim that their turnover of €514 million is the highest of any sporting club in the world after 7% (€34 million) growth from the previous year’s €480 million. However, expenses shot up €48 million with wages rising 8% (€18 million) from €216 million to €234 million and other expenses surging 26% (€30 million) to €146 million, partly due to a tax law change and higher provisions.

This meant that Madrid’s cash profits, defined as EBITDA (Earnings Before Interest, Taxation, Depreciation and Amortisation) declined from €148 million to €134 million. This is still hugely impressive, being €20 million more than Manchester United and €90 million more than Arsenal, two of England’s most financially astute clubs.

After a €5 million increase in player amortisation and depreciation, operating profit fell €19 million to €24 million, though this was boosted by €20 million profit on player sales (and other asset disposals), which was €17 million higher than the previous season. Net interest payable rose €12 million, almost entirely due to a once-off financial gain the prior year not being repeated in 2011/12.

"Casillas - number one"

This produced a profit before tax for Madrid of €32 million, which was €15 million lower than the €47 million achieved in 2010/11. This was still more than respectable, as club president Florentino Pérez affirmed, “These results are spectacular, especially given the economic circumstances we are living in.”

Barcelona’s revenue also rose 7% from €452 million to €485 million (excluding €10 million revenue from player sales), though they also managed to cut the wage bill by 3% from €276 million to €268 million. This helped increase their EBITDA by a stunning 39% from €89 million to €123 million, just €11 million behind Madrid. In fact, their lower player amortisation, arising from their policy of developing players from the La Masia academy, means that Barcelona’s operating profit of €51 million was more than twice as much as Madrid.

However, Barcelona only made a negligible €3 million profit on player sales, as the €11 million gain made from selling the likes of Jeffrén and Maxwell was almost wiped out by the €8 million loss from removing Alex Hleb, Gabriele Milito and Henrique from the books. That still represented an improvement from the previous season, when the club made an overall loss of €22 million on player sales, as the profitable sale of Yaya Touré to Manchester City was not enough to compensate for the large losses made on selling Zlatan Ibrahimovic to Milan, Dmytro Chygrynskiy to Shakhtar Donetsk, Martin Cáceres to Sevilla and Thierry Henry to New York Red Bulls.

"You've got to fight for your right to party"

Following the debt reduction, Barcelona’s net interest payable dropped €8 million to just €5 million, leading to the record €49 million profit before tax. That’s pretty impressive for a season in which Barcelona did not win the Spanish league title or the Champions League, particularly when they did not sell any players for large amounts of money. No wonder their president Sandro Rosell described this season as “excellent in terms of numbers”, though the fans might have preferred more silverware.

In fact, without the huge losses on clearing out some of the former regime’s expensive mistakes (the loss on Ibrahimovic alone was reported to be an incredible €37 million), Barcelona said they would also have made a pre-tax profit in 2010/11 of €34 million.

Actually, the picture for the football club is even better, as these figures include large losses reported for Barcelona’s other sporting activities. These amounted to €40 million in 2011/12 (basketball €22.9 million, handball €7.7 million, 5-a-side football €5.9 million, hockey €2.4 million and other sports €1.4 million), so the pre-tax profit for the football club alone would be a mighty €89 million.

It’s a similar story for Real Madrid, though unfortunately their annual report no longer analyses the profit and loss account by activity. The last report to do so (in 2008/09) listed the basketball loss as €23 million. If this were the same level today, Madrid’s profit before tax for the football club would be €55 million.

In spite of their massive expenditure, Madrid have been consistently profitable, amassing €230 million of pre-tax profits over the last six years, including €44 million in 2007, €51 million in 2008, €25 million in 2009 and €31 million in 2010. According to their annual report, the last time they reported negative EBITDA was way back in 2001/02. The club is again budgeting for a €32 million profit in 2012/13.

Barcelona’s figures have been less impressive, though they have reported profits in four out of the last six years, albeit generally much lower. The annus horribilisof 2010 with its €83 million loss was largely due to the new board taking what Javier Faus, the vice-president of economic affairs, described as a more conservative approach and booking €89 million of audit adjustments, including provisions for TV rights disputes, player transfers and land sales/valuations.

At that point, Faus admitted that Barcelona could not “allow itself to continue losing money”, leading to a more austere approach, since when substantial progress has been made on the club’s finances, resulting in this year’s mega-profits and a budgeted pre-tax profit for 2012/13 of €36 million. Nevertheless, there is no room for complacency, as Faus acknowledged, “We’re taking this with caution. We’re not euphoric. We want to wait two to three years to see if we can stabilise the trend.”

In stark contrast to the big two, very few other Spanish clubs are doing well financially. According to a study by the University of Barcelona for the 2010/11 season, only eight of the 20 clubs in La Liga were profitable – and Real Madrid were the only one of these to report a profit higher than €5 million. While the two Spanish giants gorge themselves, the other teams are starving. As Professor Gay said, “Everyone is concentrated on Madrid and Barca, who are the kings of the banquet, while the rest live an uncertain future.”

The picture is not too different on the broader European stage, as the only leading club making similar profits are Arsenal, who reported €44 million of pre-tax profits in 2011/12, though it should be noted that they would have made a €38 million loss without the benefit of €82 million of player (and property) sales, ironically including Cesc Fàbregas to Barcelona.

Bayern Munich also reported a solid profit of €9 million, the nineteenth year in succession that they have been in the black, but Manchester United slipped to a €6 million loss (before tax), dragged down by €60 million of interest charges, though in fairness they did make a €36 million profit the previous year.

At the other extreme, those clubs operating with a benefactor/sugar daddy model reported enormous losses. Manchester City’s €237 million loss in 2010/11 was the largest ever recorded in England, while Juventus, Inter, Chelsea and Milan all registered losses at around the €80 million mark.

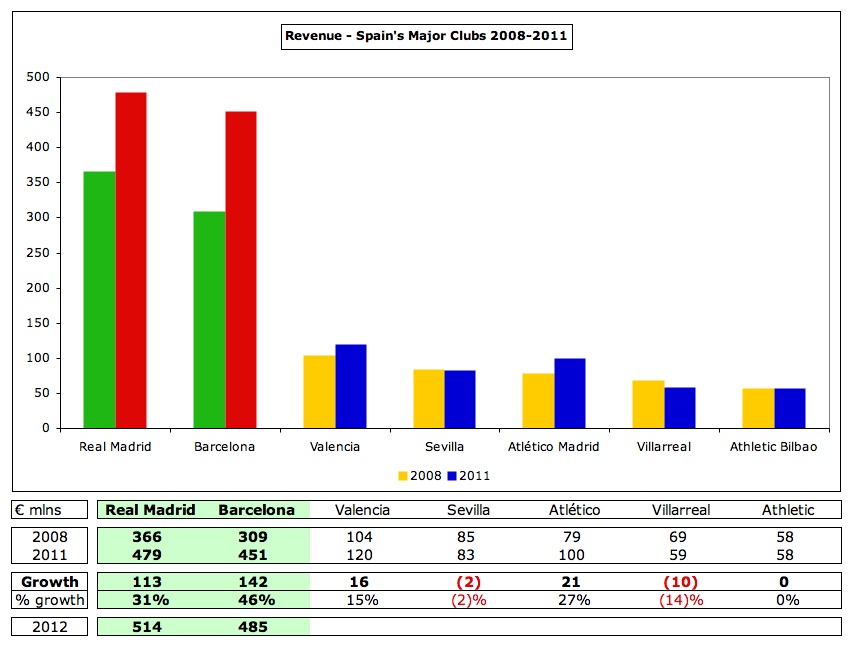

The source of Madrid and Barcelona’s financial supremacy is their astonishing ability to generate revenue. Domestically, they are so far ahead of the other clubs that it is questionable whether they are even competing in the same race. In the 2010/11 season, their respective revenue of €479 million and €451 million (very slightly adjusted to be in line with the Deloitte Money League) was around four times as much as the nearest challengers: Valencia €117 million, Atlético Madrid €100 million and Sevilla €83 million. The rest were absolutely nowhere with two of the clubs in Spain’s top division reporting annual revenue less than €10 million.

That’s bad enough, but the problem is that it’s getting worse, as only the big two have managed meaningful revenue growth over the last few years, while the others have been stagnating. In the three years between 2008 and 2011, Barcelona and Madrid increased their revenue by €142 million and €113 million respectively, while the closest to that was €21 million by Atlético Madrid and €16 million by Valencia. Athletic Bilbao’s revenue has been flat, and it has actually declined at Sevilla and Villarreal.

In 2012 it’s more of the same with the two giants both adding a further €34 million to their revenue. In short, the gap between the elite and the “working class” is already immense – and it’s getting wider every year. As Sevilla’s outspoken president José Maria del Nido said, “Revenues are making the big get bigger and others smaller.” The chances of Sevilla (or indeed anyone else) mounting a sustained challenge in Spain are virtually zero, unless one of the big two somehow implodes.

In fairness to the Spanish clubs, the theme is essentially the same in Europe with Madrid and Barcelona earning around €100 million more than the third placed club, Manchester United, and €150 million more than Bayern Munich. Their revenue is an incredible €200 million more than Arsenal, Chelsea and Milan. Moreover, they earn the highest television money and only one club betters them on commercial revenue (Bayern Munich) and one splits them on match day income (Manchester United).

Furthermore, the distance to the chasing pack is also growing year after year. Since 2005, the first year that Madrid topped the Money League, their revenue growth has been considerably higher than the other leading clubs. In that period, Madrid’s revenue rose by €204 million, while Barcelona’s growth of €243 million was even more impressive. The next highest increases were barely half that: Bayern Munich €131 million and Manchester United €121 million.

The distance to their peers has been steadily increasing from €39 million in 2009 to a staggering €130 million in 2012. In other words, everyone else has massively lost ground in relative terms. Given this significant competitive advantage, Real Madrid and Barcelona should at the very least reach the Champions League semi-finals every season (and this is indeed one of their budget assumptions).

It’s more of the same in 2012, as the Spanish leaders continued their growth story, while the only other clubs to publish their results for last season either only grew slightly (Arsenal) or even fell back (Manchester United – due to earlier elimination in the Champions League).

Part of the widening disparity reported in 2011 was down to currency movements, as the exchange rate that Deloitte used for their last publication was 1.11 Euros to the Pound. Since then, the Euro has weakened, but even if we apply the current exchange rate of 1.25, the picture is basically unchanged. Since 2009, the growth rate at Barcelona (€119 million) and Real Madrid (€113 million) has been at least twice as fast as their nearest rival (Manchester United €52 million). Of course, Bayern and Chelsea have yet to publish their 2012 figures, but that is unlikely to significantly distort the picture.

We should note that both clubs have provided moderate revenue projections for the 2012/13 season: flat for Madrid, as lower revenue from the summer tour (because of Euro 2012) is compensated by growth in other areas; and a 5% decrease for Barcelona, partly due to no European Super Cup or Club World Cup, with Faus admitting, “Each year it’s harder to find new revenue streams.” However, it should also be acknowledged that they have often managed to beat their revenue budget in previous years.

One other positive aspect of their revenue is how evenly balanced it is between the three revenue streams. The split is almost identical: broadcasting – Madrid 38%, Barcelona 40%; commercial – Madrid 36%, Barcelona 35%; match day – Madrid 26%, Barcelona 25%. As Madrid’s annual report puts it, this diversified structure provides economic stability, cushioning the impact of potential revenue fluctuations arising from sporting factors or the prevailing economic conditions.

Even though they have been remarkably successful in producing a balanced revenue model, broadcasting revenue still provides them with a key competitive advantage over their foreign counterparts, thanks to their lucrative domestic deal. Unlike all the other major European leagues which employ a form of collective selling, Spanish clubs uniquely market their broadcast rights on an individual basis, so Madrid and Barcelona each received €140 million in 2011/12, which was three times as much as the nearest competitors, Valencia €48 million and Atletico Madrid €46 million, followed by Sevilla €31 million and Betis €29 million.

In other words, Madrid and Barcelona on their own received around 43% of the total TV money in La Liga or 11 times as much as the €13 million given to the last club on the list (Racing Santander). This unbalanced deal produces the most uneven playing field in Europe and compares unfavourably to the 1.6 multiple in the Premier League between first and last clubs. Such a revenue disadvantage is bad enough for one season, but it makes a gigantic difference over time. As Sevilla president del Nido complained, “The two giants have earned €1,500 million more than the next club in the last ten years.”

Looked at another way, they received about twice as much from their domestic deal as Premier League champions Manchester City, though the gap should be halved from the 2013/14 season when the new English contract kicks in. In fact, their TV revenue is more than the total revenue of all but eight other clubs.

Both clubs have TV agreements in place until 2014/15, which highlights one potential problem, as the rights holder Mediapro has experienced severe difficulties leading to the company seeking bankruptcy protection over a dispute with Sogecable. Furthermore, other TV channels have spoken of not bidding for rights for matches in future, due to the high price and depressed advertising market. That probably explains why Faus admitted, “Media income has peaked and we don’t expect increases in the next five years.”

"Every little thing he does is magic"

However, the strongest threat to this revenue stream is the other clubs’ desire to move to a collective structure, as summarised by Atlético Madrid’s president Miguel Ángel Gil Marín, “We want a league that is solvent and competitive. To achieve that, it is fundamental that the gap in budgets and revenues is narrowed and there is a fairer distribution of TV rights.”

To date, this has been staunchly resisted by Madrid and Barcelona, but Spain’s sports minister José Ignacio Wert believes that they are now “receptive” to the idea of a more equitable distribution. Indeed, last year Sandro Rosell said, “The television rights are negotiated individually now, but in three, four, five years’ time, we will have to put them all in one pot and make La Ligaas it is in Italy and the Premier League”, though his price is a reduction in the number of clubs from 20 to 16.

That might sound like yet another slice of “pie in the sky”, but there are reasons to believe that this might happen, not least that collective agreements tend to be worth more than the sum of their parts. La Liga’s TV rights revenue of €655 million is a long way behind the Premier League’s current €1.4 billion (rising to an estimated €2.2 billion in 2014). In fact, they have now been overtaken by the Bundesliga(€0.7 billion) and Serie A, whose return to a collective deal helped grow TV rights to just under €1 billion.

That is a huge prize to go after, especially overseas rights, which is the reason why so many in Spanish football are now actively pushing to make the “product” more attractive to viewers abroad, as articulated by former Real Madrid legend Emilio Butragueño, “We want … a brand like the Premier League. The best players in the world are here in Spain and we have to profit from it.” Of course, that is easier said than done, especially in the current harsh economic environment.

TV money has been boosted by participation in the Champions League with both Madrid and Barcelona receiving around €40 million last season from the central distribution. This again drives a wedge between them and other Spanish clubs, as the less successful Valencia (€19 million plus €3 million for parachuting into the Europa League) and Villarreal (€14 million) earned much less. It was even worse in the Europa League, as Atlético Madrid and Athletic Bilbao only earned around €10 million, even though they both reached the final.

Barcelona have consistently earned more money from Europe’s flagship tournament than Madrid, thanks to their superior results, notably the €51 million garnered when they won the trophy in 2010/11. That said, Madrid’s improved performances under José Mourinho have resulted in revenue rising €12 million to €38-39 million in each of the last two seasons. The Champions League bonanza shows little sign of slowing down, as the prize money for the 2012 to 2015 three-year cycle has increased by 22%.

Both clubs have adopted a strong commercial philosophy. Marcel Planellas of the famous Easde business school compared Barcelona’s strategy to a movie studio, “Just like Disney, you’ve got your stars, your world tours, the box office, the television rights, the t-shirts and all the other merchandising.” That description could equally apply to Real Madrid, who have recently announced plans to build a $1 billion “football island” holiday resort in the United Arab Emirates to strengthen their presence in the Middle East and Asia.

In 2010/11, their commercial revenue (Madrid €172 million, Barcelona €156 million) was only surpassed by Bayer Munich’s barely credible €178 million, but was a fair way ahead of other clubs with Manchester United being the nearest at €114 million. In Spain, it’s less of a gap to the next clubs, more of an abyss with the difference being at least €125 million to Atlético Madrid €29 million and Valencia €23 million. Note that Deloitte appear to have re-classified membership fees to commercial income in their analysis.

Perhaps unsurprisingly, the shirt sponsorship and kit supplier deals are the highest in football. Barcelona’s five year deal with Qatar Foundation, running until 2015/16, is worth €30 million a year (plus €15m for “commercial rights” in 2010/11) and is their first ever paid shirt sponsorship. Rosell argued this was due to the arrival of wealthy owners at other clubs, “If we did not have to fight against competition which has capital, I would never sell anything on the shirt.” Madrid’s agreement with Bwin, reportedly also worth €30 million, runs until 2012/13.

It’s not so rosy at other Spanish clubs with almost half of the clubs in La Ligastarting last season without a shirt sponsor, including Valencia, Sevilla and Villarreal. However, the bar is continually being raised at the leading clubs with Manchester United recently announcing a spectacular deal with Chevrolet, which will be worth an astonishing €56 million from 2014/15.

For kit suppliers, Madrid have just extended their deal with Adidas to 2019/20 for €38 million, while Barcelona renewed their Nike deal in 2008 for €33 million to 2012/13 (with an option to extend to 2018). The closest to them are Manchester United (Nike) and Liverpool (Warrior), who both earn around €32 million. An indication of Madrid’s commercial strength came from the five-year secondary sponsor deal that Emirates Airlines signed for €5 million a season, purely for some “prominent” advertising space within the ground.

In terms of shirt sales, a survey by PR Marketing suggested that Madrid and Manchester United lead the way with annual sales of 1.4 million, followed by Barcelona with 1.15 million.

Commercial income has also been helped by uplifts from success like winning the Champions League and other activities, e.g. stadium tours, ticket exchanges, though there are limits with both clubs unwilling to play the Spanish Super Cup in China. Indeed, Faus cautioned, “advertising is not immune to the current economic climate.”

Stop me if you’ve heard this one before, but Madrid and Barcelona are also at the top of the league for match day income: in 2010/11 Madrid were first with €124 million and Barcelona third with €111 million. The next highest in Spain were again miles behind: Atlético Madrid €30 million, Valencia €27 million and Athletic Bilbao €25 million. This figure is impacted by the number of matches played, e.g. progress in Europe, and other events, such as Madrid hosting the Champions League final in 2010.

In recent years, the clubs have avoided raising ticket prices too much. Indeed, Barcelona’s new board promised not to increase them for two years, which they extended an additional year for the 2012/13 season. However, there are hints that this may change with Faus talking about wanting “to have a debate” on prices.

Both clubs also benefit from membership fees with Barcelona reporting revenue of nearly €20 million from their 170,000 members. Madrid do not explicitly break out their income, though they do list the fees paid by their 93,000 members, implying revenue of €10 million.

Attendances are among the highest in Europe with Barcelona overtaking Madrid three years ago, though their crowds fell last season to 76,000, around 1,000 more than their great rivals, even though Faus said that “ticket sales have been spectacular.” One caveat here is that Spanish attendance figures are notoriously inaccurate, as explained in this interesting article from Estadios de Fútbol en España.

Last month both clubs made announcements regarding possible stadium development. Madrid unveiled four models to “turn the Bernabéu into a world class arena”, which would cost €250 million, according to El Pais, and take three years with the work starting next summer. Just two months after Rosell said that Barcelona would put planned stadium renovations on hold until the club’s debt had been further reduced, he announced a referendum whereby members could decide whether to: leave the Nou Camp unchanged; redevelop it (last year there were plans to add 10,00 seats and install new VIP boxes); or build a new stadium. Faus indicated that redevelopment would cost €300 million, while a full stadium move would be €600 million.

It is clear that both clubs have made efforts towards cost containment. In particular, Barcelona cut their wage bill from €241 million to €233 million in 2012. This gave some support to Rosell’s claim that “austerity will be a pillar of our day-to-day management”, though sporting salaries still rose by €17 million to €155 million, following the arrival of Fàbregas and Alexis Sánchez. This was off-set by a €24 million reduction in bonus payments to €44 million, as the club failed to retain La Liga and the Champions League.

In fairness, the wages to turnover ratio has improved from 59% in 2010 to a very creditable 48% in 2012, though Faus conceded that “it’s difficult to reduce the (wages) figure further and still maintain stability.”

As a technical aside, I have used the wages from Barcelona’s detailed accounts here to be consistent with the University of Barcelona analysis. The business review section of Barcelona’s annual report lists salary costs as €268 million (sports €237 million, other €31 million), as this also includes other costs, mainly image rights of €24 million.

In contrast to Barcelona, Madrid’s wage bill rose from €216 million to €234 million (almost identical to their rivals), presumably due to bonus payments for winning the league, though they managed to maintain their superb wages to turnover ratio at 46%. This may come under pressure from the abolition of the so-called “Beckham Law”, which allowed foreigners to benefit from a lower tax rate. As many players, such as the occasionally “sad” Ronaldo, are paid net, the club potentially faces a sizeable increase in its costs from 2015, when the tax rate increases from 24% to 52%.

Again, these wage bills are considerably higher than other Spanish clubs – at least €150 million higher in 2010/11 with Atlético Madrid and Valencia the closest at just €64 million and €61 million respectively. Some of the comparatives are almost laughable, e.g. Levante’s wage bill of €7 million is about 3% of Madrid’s.

As with revenue, it’s getting worse for the rest of Spain with the wages gap ever widening. Between 2008 and 2011 Barcelona’s wage bill rose €72 million, while Madrid’s increase by €49 million. In the same period, the wage bills at Atlético Madrid, Valencia and Sevilla actually fell, while Bilbao’s €14 million growth only took them to €49 million.

Their wages are also the highest in Europe, though Manchester City and Chelsea were quite close with €209 million and €202 million respectively. However, there are a couple of caveats. First, the exchange rate can play a part, so City would have been higher than Madrid in 2010/11 at today’s rates. Second, both Spanish clubs’ wage bills are inflated by other sports. In Barcelona’s case, this amounted to €31 million in 2011/12, while Madrid included around €23 million. Barca have targeted these for future savings.

Despite this factor, Madrid’s wages to turnover ratio of 45% was still better than both the financially prudent clubs (Manchester United 46%, Bayern Munich 49%, Arsenal 55%) and the more profligate ones (Manchester City 114%, Inter 90%, Milan 88%, Chelsea 75%).

The other expense impacted by investment in the squad, player amortisation, rose last year at both clubs: from €92 million to €98 million at Madrid and from €56 million to €61 million at Barcelona. For non-accountants, amortisation is simply the annual cost of writing-down a player’s purchase price, e.g. Karim Benzema was signed for €35 million on a six-year contract with the transfer reflected in the accounts via amortisation, which is booked evenly over the life of his contract, so around €6 million a year.

The only other major football club with similarly high player amortisation to Madrid is Manchester City with around €100 million. The €37 million difference with Barcelona highlights their different approaches: Madrid tend to buy in their stars, while Barcelona look to develop their youngsters in-house. As Faus said, “There’s no need to spend €80 million, as we have La Masia”, which has produced Xavi, Iniesta and Lionel Messi (among many others).

This can be seen by the net transfer spend: in the last seven years, Madrid’s €477 million was almost 80% higher than Barcelona’s €266 million. That said, there has been a sea change at Madrid with a distinct slowing-down in the last three years, with net spend of “only” €128 million compared to €349 million in the previous four years, when they launched the second version of the Galácticosproject, buying Ronaldo, Kaká, Xabi Alonso and Benzema. It’s a similar story at Barcelona where they have spent just €65 million (net) in the past three years, less than a third of their €202 million outlay in the previous four years.

Faus has said that Barcelona’s average annual budget for new signings will be €40 million. He added that any over-spend would be compensated in future years, “Last year we surpassed our transfer budget with the signings of Cesc Fàbregas and Alexis Sánchez. We cannot overspend our budget by 20 or 30 million euros each year, it would put our business plan at risk. It wouldn’t be sustainable.”

Even with this more reasonable approach, the big two continue to outspend the other Spanish clubs. In the last three years, most have actually made money in the transfer market: Valencia €62 million, Athletic Bilbao €27 million, Atlético Madrid €19 million and Sevilla €5 million. The only leading club with a net spend is Malaga and that looks like a temporary blip after their ownership problems.

Transfer spending was down 70% in La Liga this summer to just €116 million with over half coming from Madrid and Barcelona (on Luka Modric, Alex Song and Jordi Alba). Some clubs didn’t spend a single Euro on player recruitment.

Given their financial weaknesses (and inability to compete), the other Spanish clubs are effectively forced to sell their stars, thus creating a vicious circle where the dominance of Madrid and Barcelona becomes more firmly entrenched. As an example, in the past few years, Valencia have lost David Villa, David Silva and Juan Mata, while Atlético Madrid have sold Sergio Aguero, Diego Forlán and David de Gea. They either move abroad or actually join Madrid or Barcelona.

Where the Spanish giants have to be careful is that they are no longer the only game in town. In fact, over the last three years they have been outspent by new money, particularly Chelsea (€272 million), Manchester City (€244 million), Paris Saint-Germain (€242 million) and Zenit Saint Petersburg (€151 million). Money talks, but oil money talks louder.

The most worrying issue for the Spanish giants, widely reported in the media, has been their large debts, though this is open to interpretation (as explained in this earlier blog). The press tend to use the broadest possible definition of debt, namely total liabilities, which includes trade creditors, accruals and even provisions. In 2012 this gives enormous headline figures for Madrid and Barcelona of €590 million and €471 million respectively. To place that into perspective, is the same measure were to be applied to English clubs, Arsenal, universally applauded for their financial prudence, would have “debt” of €585 million, about the same as Madrid and more than Barcelona, while Manchester United are much higher at €890 million.

Under the more standard definition of net debt, Madrid’s balance is only €30 million (bank loans of €143 million less cash €113 million), while Barcelona have €99 million (gross debt €136 million less cash €37 million). Both of these are lower than Arsenal (€124 million) and Manchester United (a hideous €458 million). However, Madrid also have significant net transfer liabilities owed to other football clubs (included in UEFA’s debt definition) of €55 million.

In 2010/11 Madrid (€590 million) and Barcelona (€578 million) had the highest debts in Spain, but this is cushioned by very good debt coverage (revenue/debt) of around 80%. This ratio highlights the bigger debt challenges faced by other clubs such as Atlético Madrid (debt €514 million, cover 19%) and Valencia (debt €382 million, cover 31%), though a promising sign came last month from Miguel Cardenal, Spain’s secretary of sport, who said that football club debts were declining for the first time in decades.

Madrid have succeeded in slashing debt from €327 million in 2009 to €125 million in 2012, largely because of a significant reduction in transfer liabilities. This is under their own definition, which is essentially the same as UEFA’s (bank debt plus net transfer fees payable) plus selected creditors (essentially stadium debt).

Similarly, Barcelona have cut debt by 22% in two years from €430 million to €334 million, again using an in-house definition. This is a fine achievement, considering the issues in 2009, when the club had to seek an emergency €155 million to overcome short-term cash flow problems, including paying the players. Faus has admitted that the debt is “still too high for us to be able to dictate our future” and the club’s strategic plan aims to reduce the balance to €190 million by 2015/16.

Madrid’s balance sheet is quite strong with €275 million of net assets, which is much better than Barcelona’s net liabilities of €20 million (though this has improved €49 million in 2012). However, Barcelona have “hidden” assets, as the players are only included in the accounts at book value of €143 million, while Transfermarktestimates their real market value at a mighty €601 million.

Based on their strong financial performance in 2011/12, UEFA’s Financial Fair Play (FFP) regulations, which force clubs to live within their means if they wish to compete in Europe, should not prove overly problematic for Madrid and Barcelona. The allowable losses are an aggregate €45 million for the first two years (then three years), but this is only €5 million if losses are not covered by the owners, which might be more relevant here, given that the clubs are owned by their members.

In any case, they can exclude certain expenses, including depreciation on tangible fixed assets and expenditure on youth development and community activities, which would be worth at least €20 million. On top of that, they could argue that losses made by other sports should also be ignored, though the FFP guidelines suggest that “other sports teams” might be included.

Perhaps the biggest threat to the financial ascendancy of Madrid and Barcelona is the desperate situation of Spanish football in general. Even though results on the pitch have never been better for the Spanish national team and their clubs in Europe (five of the eight semi-finalists in Europe last season came from La Liga), most clubs are struggling off the pitch with a quarter of the clubs in the top division in bankruptcy protection. As Professor Gay said, “Many clubs are living dangerously.”

"So why so sad?"

The start of last season was delayed by a players’ strike over unpaid wages and there were threats of similar this season, this time over TV rights and schedules. This is exacerbated by the desperate state of the Spanish economy, which is firmly in recession with unemployment running at a record 23%.

With their new found focus on sustainability, Madrid and Barcelona will be fine from a financial perspective, but it is conceivable that fans may lose interest in La Liga, due to the lack of competition. The financial disparity with the rest of the league was always large, but it has become colossal, leading to doubts about some clubs’ ability to survive. Professor Gay warned, “If things go on like this, Spanish football will kill itself.”

At the moment, Madrid and Barcelona give the impression of fiddling while the rest of the country burns, but they would do well to remember the wise words uttered in Spider-Man (or, if you prefer, the works of Voltaire), “with great power comes great responsibility.”